- “EU–Australia FTA: Strategic Implications for Global Commodity Competition

Where the EU–Australia agreement stands

• Status: The EU and Australia have been negotiating a free trade agreement (FTA) since 2018; talks have been difficult mainly over agriculture (beef, sheep meat, sugar, dairy, grains, GI protection).

• Strategic aim: For both sides, it’s about securing supply chains, diversifying partners away from over‑dependence on China, and locking in rules-based trade in services, investment, and standards.

• Agriculture sensitivity: Agriculture is the most politically sensitive chapter—exactly where the competitive overlap with Mercosur and some ASEAN exporters is strongest.

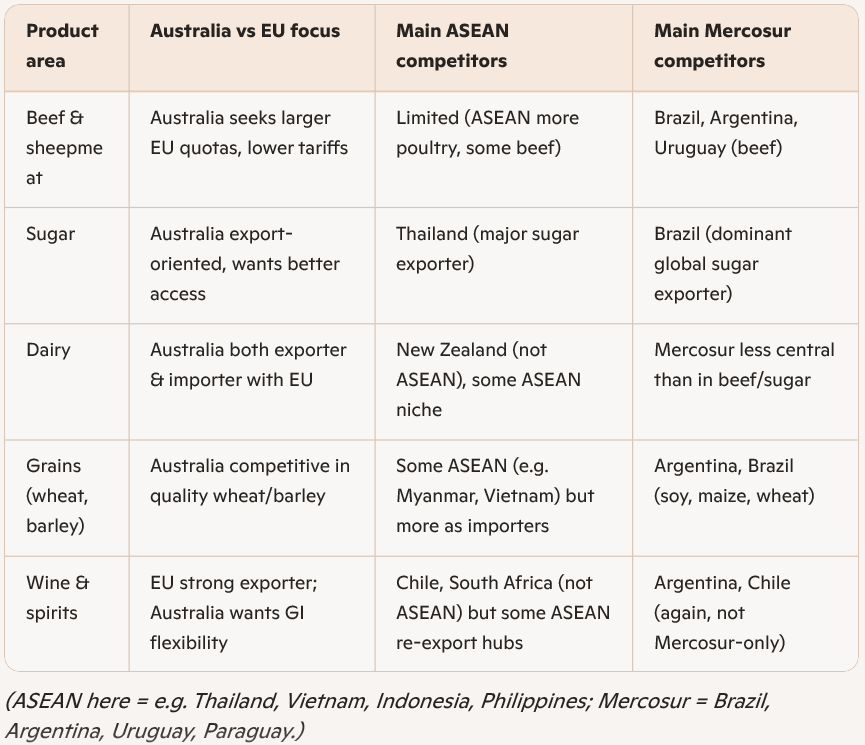

2. Key commodities: EU–Australia vs ASEAN and Mercosur

3. Likely consequences on commodities if the EU–Australia FTA is concluded

3.1 For Australia in the EU market

• Beef and sheep meat:

• If quotas/tariffs improve: Australian beef and lamb become more competitive in high‑value EU segments (premium cuts, grain-fed beef).

• Competitive impact:

• Mercosur: Brazil/Argentina currently dominate EU beef import quotas; extra Australian access would directly eat into their market share in some segments, especially if Australia can brand on sustainability and traceability.

• ASEAN: Limited direct competition in beef; ASEAN is more important as a destination for Australian beef than as a competitor in the EU.

• Sugar:

• If EU grants meaningful tariff‑rate quotas (TRQs): Australian raw sugar could compete more directly with Brazilian and Thai sugar in EU refining and industrial use.

• Competitive impact:

• Mercosur: Brazil is the global price setter; any Australian access to the EU is small in volume but strategically diversifies EU away from Brazil.

• ASEAN: Thailand is the key competitor; an FTA could shift some EU demand from Thai to Australian sugar if preferences are significant.

• Grains (wheat, barley, possibly pulses):

• If tariffs are reduced: Australia can position itself as a reliable, high‑quality supplier for milling wheat and malting barley.

• Competitive impact:

• Mercosur: Argentina and, to a lesser extent, Brazil compete in wheat and maize; Australian access would intensify competition, especially in quality‑sensitive segments (milling, malting).

• ASEAN: Mostly importers; not a major competitive threat in the EU for grains.

• Wine and high‑value food products:

• Tariff cuts: Help Australian wine, processed foods, and niche Agri‑products in the EU retail and HoReCa segments.

• Competition: More with EU internal producers and New World exporters than with ASEAN/Mercosur, but Mercosur (Argentina, Chile) competes in some wine categories.

3.2 For the EU in the Australian and regional markets

• Dairy, processed foods, beverages:

• EU exporters gain better access to Australia: Cheese, specialty dairy, processed foods, and beverages become more competitive versus New Zealand, US, and some ASEAN suppliers.

• Spillover into ASEAN: Stronger EU–Australia value chains (e.g. EU ingredients processed in Australia, then re‑exported to Asia) could indirectly increase EU presence in ASEAN markets.

• Industrial goods and green tech:

• EU advantage: Machinery, vehicles, renewable energy tech, and chemicals gain from tariff cuts and regulatory cooperation.

• Commodities link: This strengthens EU’s position in supplying equipment for Australian mining and agriculture, indirectly affecting cost structures of Australian commodity exports competing with Mercosur/ASEAN.

4. Interaction with ASEAN and Mercosur in key product markets

4.1 Beef and meat markets

• EU import side:

• Mercosur vs Australia: Any additional Australian beef quota in the EU will likely be politically balanced by limits on Mercosur concessions, or vice versa, because EU farmers see both as competitive threats. The EU’s own impact studies show beef as one of the most negatively affected sectors from FTAs with both Mercosur and Australia.

• Result: A concluded EU–Australia FTA with meaningful beef access would sharpen competition with Mercosur suppliers for high‑value EU beef demand.

• Asia-Pacific side:

• ASEAN as destination: Australia, New Zealand, and increasingly Brazil supply beef to ASEAN markets. If Australia diverts some high‑value cuts to the EU thanks to better access, Mercosur (especially Brazil) could fill more of the price‑sensitive ASEAN demand.

4.2 Sugar and bioenergy

• EU import side:

• Brazil & Thailand vs Australia: If the EU grants Australia preferential access for sugar, it slightly reduces the relative advantage of Brazil and Thailand in the EU market.

• Strategic angle: EU may use Australian sugar as a diversification tool to avoid over‑reliance on Brazil, especially in a context of sustainability and deforestation concerns.

• Global competition:

• Mercosur (Brazil): Still the volume and price leader; Australian gains in the EU would be marginal in global terms but symbolically important.

• ASEAN (Thailand): Faces preference erosion if Australia gets lower tariffs or TRQs.

4.3 Grains and oilseeds

• EU import side:

• Australia vs Mercosur:

• Australia is strong in wheat and barley; Mercosur in soy, maize, and some wheat.

• Preferential access for Australian grains would intensify competition with Argentina in particular for EU milling wheat and barley niches.

• ASEAN angle:

• ASEAN is more a buyer than a competitor in grains; the main effect is indirect—if Australia finds better margins in the EU, it may rebalance flows between EU and Asian markets, leaving space for Black Sea or Mercosur origins in ASEAN.

5. Strategic consequences and positioning

• For the EU:

• Diversification: An FTA with Australia helps diversify away from single‑supplier dependence (e.g. Brazil for beef/sugar, US for some grains), while still protecting sensitive sectors via quotas and safeguards.

• Standards leverage: The EU can export its regulatory model (sustainability, animal welfare, GIs), which may raise compliance costs for all suppliers—Australia, Mercosur, and ASEAN alike—but could favour those who adapt fastest.

• For Australia:

• Upgrading market mix: Better EU access lets Australia shift more volume into high‑value, high‑standard markets, reducing vulnerability to political shocks in China and price competition in ASEAN.

• Competitive edge vs Mercosur/ASEAN:

• In beef, lamb, sugar, grains, Australia can market itself as a “clean, green, traceable” supplier aligned with EU standards, which is harder for some Mercosur and ASEAN producers facing deforestation or labour‑standard scrutiny.

• For ASEAN and Mercosur:

• Mercosur: Faces tighter competition in EU beef, sugar, and some grains if Australia gets meaningful preferences; political resistance inside the EU may force trade‑offs between concessions to Mercosur and to Australia.

• ASEAN: More affected in sugar (Thailand) and some processed foods; otherwise, the impact is indirect—through trade diversion and value‑chain reconfiguration rather than head‑to‑head competition in the EU.